The 2026-27 Federal Budget is focused on stabilising the Australian economy amid global oil supply shocks caused by conflict in the Middle East, alongside domestic issues of high inflation, weak productivity growth and high wealth inequality. Here, the government is attempting to balance competing economic objectives including price stability, sustainable economic growth, equity in the distribution of income and wealth, and environmental sustainability.

To understand the implications of the budget for the Australian economy, it’s important to consider the overall budget outcome and stance, and the difference between these concepts:

- The budget outcome is the government’s revenue minus the government’s expenditure over the financial year

- The budget stance examines how this outcome has changed compared to the previous year

The budget outcome is projected to be a deficit of $31.5 billion, or around 1% of GDP in 2026-27. This is slightly larger than the previous year’s deficit of $28.3 billion, yet remains stable as a proportion of GDP, suggesting a neutral fiscal stance.

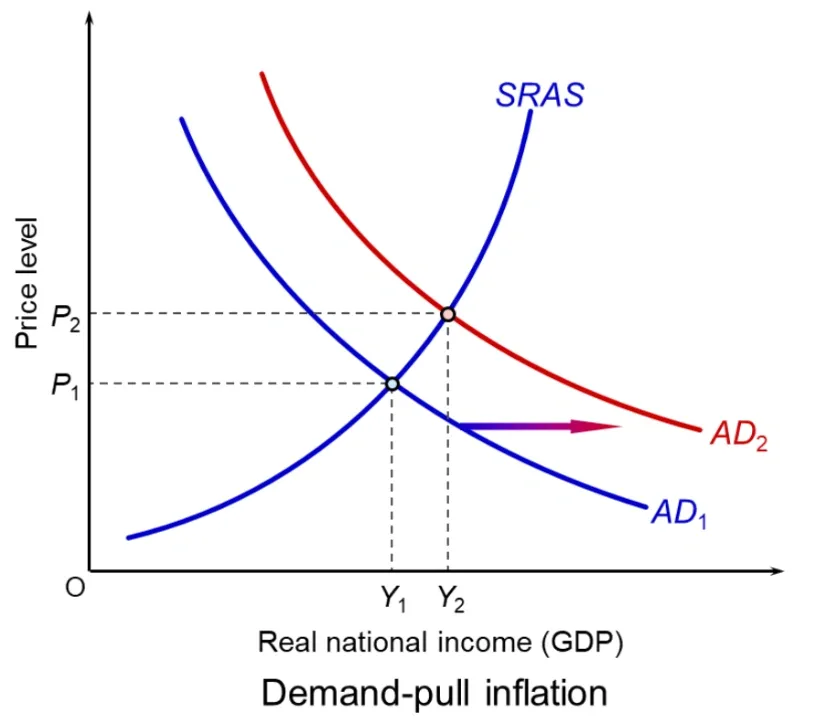

Fiscal policy is important because it directly impacts aggregate demand (AD = C + I + G + (X - M)) through changes in net government expenditure (G). As we know, aggregate demand and aggregate supply determine economic growth. Expansionary fiscal measures, such as higher government spending and lower taxation, can increase aggregate demand, thereby stimulating economic growth and reducing cyclical unemployment through the derived demand for labour. However, if aggregate demand rises faster than aggregate supply, excess demand can lead to demand-pull inflation, as consumers compete for limited goods and services, pushing prices higher. This makes a neutral stance important to avoid exacerbating existing inflationary pressures, with inflation currently projected at 5% in the year to the 2026 June Quarter, well above the ideal rate of 2-3%.

Source: Pearson, Budget 2026-27, 2025-26 MYEFO, CommBank

Nevertheless, the continued deficit, including income tax relief and infrastructure spending, suggests fiscal policy will still have a mild role in stimulating aggregate demand and potentially adding to demand-pull inflationary pressures.

To better understand the likely impacts of this year’s budget, we need to examine the major policy decisions and how they relate to the HSC Economics Syllabus:

- Wealth Tax

- Productivity

- Fuel Security

- Environmental Sustainability

- Income Tax Relief

- NDIS & Social Services

1. Wealth Tax

One of the most transformative parts of this budget is the overhaul of wealth taxation to reduce inequality in the distribution of income and wealth and improve housing affordability.

1.1. Capital gains tax

Capital Gains Tax (CGT) is taxation on the profits earned from selling assets. Since 1999, Australia has applied a 50% CGT discount to assets held for more than 12 months.

However, from July 2027, the CGT will be discounted based on inflation, meaning the original purchase price of an asset will be indexed to inflation before the taxable gains are calculated.

Additionally, a minimum 30% tax rate will apply to all capital gains. This is designed to eliminate the practice of strategically selling assets during low income years, such as retirement, where they would otherwise face a lower marginal tax rate.

The policy will be gradually introduced, applying only to gains accrued from July 2027 and several exemptions remain. As before, primary residences will remain exempt from CGT. Importantly, investors in new builds which genuinely increase the housing supply will be able to choose between the old and new CGT system, allowing them to pay whichever results in a lower tax burden.

Overall, this reform reduces tax advantages for investment into existing property while encouraging investment into new housing supply.

1.2. Negative gearing

The government is also restricting negative gearing. Negative gearing occurs when the costs of an asset, such as mortgage interest payments and maintenance expenses on a rental property, exceed the income earned. Currently, investors can deduct these losses from their taxable income, reducing income tax paid.

Under the new policy, existing assets can still be negatively geared until they are sold. However, assets purchased between the budget announcement and the 30th of June 2027 will be eligible for negative gearing only during that period, and assets purchased after that date cannot be negatively geared. Nevertheless, like the CGT reforms, an exemption applies to new builds, which will still be able to be negatively geared.

—

The main objective of these reforms is to reduce inequality in the distribution of income and wealth in Australia. Firstly, we need to distinguish between these two types of inequality:

- Wealth inequality refers to the gap in the value of assets held by households across the economy. High wealth inequality leaves poorer households financially vulnerable during high inflation periods, as their savings decline in value, and during economic downturns, as they have a reduced safety net.

- Income inequality refers to inequality in the flow of income to different households. High income inequality constrains consumption and therefore short term economic growth, as money is directed away from low income earners with a high Marginal Propensity to Consume (MPC). This inequality further increases fiscal burdens through the need for transfer payments to support low income individuals.

Existing negative gearing and CGT discounts perpetuate both wealth and income inequality. Firstly, they have made property investment highly attractive, creating high demand. As we know, when demand outpaces supply, prices rise, making it more difficult for first home buyers to enter the market, leading to inequality in wealth distribution. By altering tax incentives to reduce investor demand for existing properties and increase housing supply, the government is seeking to reduce prices to make home ownership more accessible. It is projected that the reforms could cause an additional 75,000 Australians to become homeowners, and slow house price growth by 2 percentage points over two years. Further, by increasing taxation on income earned from assets, these reforms reduce the disposable incomes of high wealth holders, decreasing income inequality.

However, there are mixed views on how effective these reforms will be in achieving Australia’s economic objectives.

The gradual implementation of the policies, including the continued ability for investors to negatively gear properties already owned, constrains the short to medium term impacts of the policy on housing supply and inequality. This demonstrates political constraints on fiscal policy, as the government must balance the need to maintain voter support amongst existing wealth holders.

Additionally these reforms may discourage rental property investment, reducing rental supply and increasing rental prices, disproportionately harming low-income renters. However, the Treasury forecasts this effect will be limited, with only a $2 increase in weekly median rental prices.

There are also concerns for innovation and business activity, as higher CGT rates may reduce the attractiveness of employee share schemes commonly used by start-up businesses to attract skilled workers by allowing them to acquire equity into the company which can be sold for capital gains in the future. This could weaken domestic entrepreneurship and innovation, limiting Australian aggregate supply and therefore economic growth.

Sources: Budget 2026-27, Australian Financial Review, ABC, ABC, ABC, Poverty and Inequality

1.3. Discretionary trusts

The government is also implementing changes to discretionary trusts.

Discretionary trusts allow a trustee to distribute income from the trust between beneficiaries each year. Currently, trust income is paid at the rate of each beneficiary’s MRT, meaning income can be distributed to low income individual beneficiaries and corporate beneficiaries reducing tax paid on the trust income.

However, from July 2028, trust income will be taxed at a minimum 30% tax rate before being distributed. Beneficiaries at a higher effective MRT will then owe the additional percentage.

This increase in taxation of discretionary trust incomes will also improve wealth and income inequality, as 90% of total private trust wealth is concentrated with the wealthiest 10% of households.

However, 350,000 Australian small businesses use a discretionary trust structure to distribute profits and minimise taxation. Higher taxation may reduce profitability and therefore business activity, also limiting aggregate supply and further slowing economic growth.

Sources: Budget 2026-27, Australian Financial Review, ABC

2. Productivity

The government has introduced a package of policies aimed at increasing productivity.

Productivity refers to the amount of output produced per unit of input. When productivity rises, the economy can produce more goods and services from the same resources, increasing aggregate supply and lowering unit production costs. This supports sustainable economic growth while reducing cost-push inflationary pressures. In the longer term, higher productivity can also support real wage growth, improve living standards, reduce cyclical unemployment and increase government tax revenue. However, because productivity improvements usually require structural changes such as investment in skills, technology, capital and infrastructure, these benefits are typically achieved in the medium to long term.

Australia’s productivity growth has been weak, averaging just 0.8% per year in the two decades to 2023–24. As a result, the RBA estimates that the Australian economy can grow by only around 2% per year without generating inflationary pressures. This is because when aggregate demand increases without a corresponding increase in aggregate supply, excess demand can emerge, leading to demand-pull inflation.

Key reforms implemented in the new budget include reducing financial sector compliance costs by $780 million, and removing 497 ‘nuisance tariffs’ from July 2026. ‘Nuisance tariffs’ are those taxes on imports which generate minimal revenue and provide limited domestic protection, yet create substantial compliance costs. By reducing regulatory burdens on firms, resources can be allocated more efficiently for productive uses.

The government is also incentivising innovation, including implementing a permanent $20,000 instant asset write-off for small businesses to encourage capital investment, and providing up to $70 million in ‘AI Accelerator’ grants to support technological development. These policies increase technical efficiency, which refers to the ability to maximise output with minimum average costs.

The budget also includes a $85.2 million investment into accelerating migrant skills recognition, alongside plans to reform the skilled migration points test to select highly educated, highly skilled and younger migrants, improving labour productivity.

Overall, the government projects their reforms to reduce regulatory burdens by $10.2 billion and boost long-run GDP by $13 billion annually - suggesting its value in improving Australian productivity to achieve heightened economic growth, price stability and better fiscal outcomes.

However, productivity challenges remain structurally embedded in the Australian economy, with recent Treasury projections that productivity growth will not rise to its long term average rate of 1.2% until the early 2030s. This suggests that these reforms are unlikely to fully redress these challenges in the short term.

Sources: Budget 2026-27, Australian Financial Review, Reserve Bank of Australia

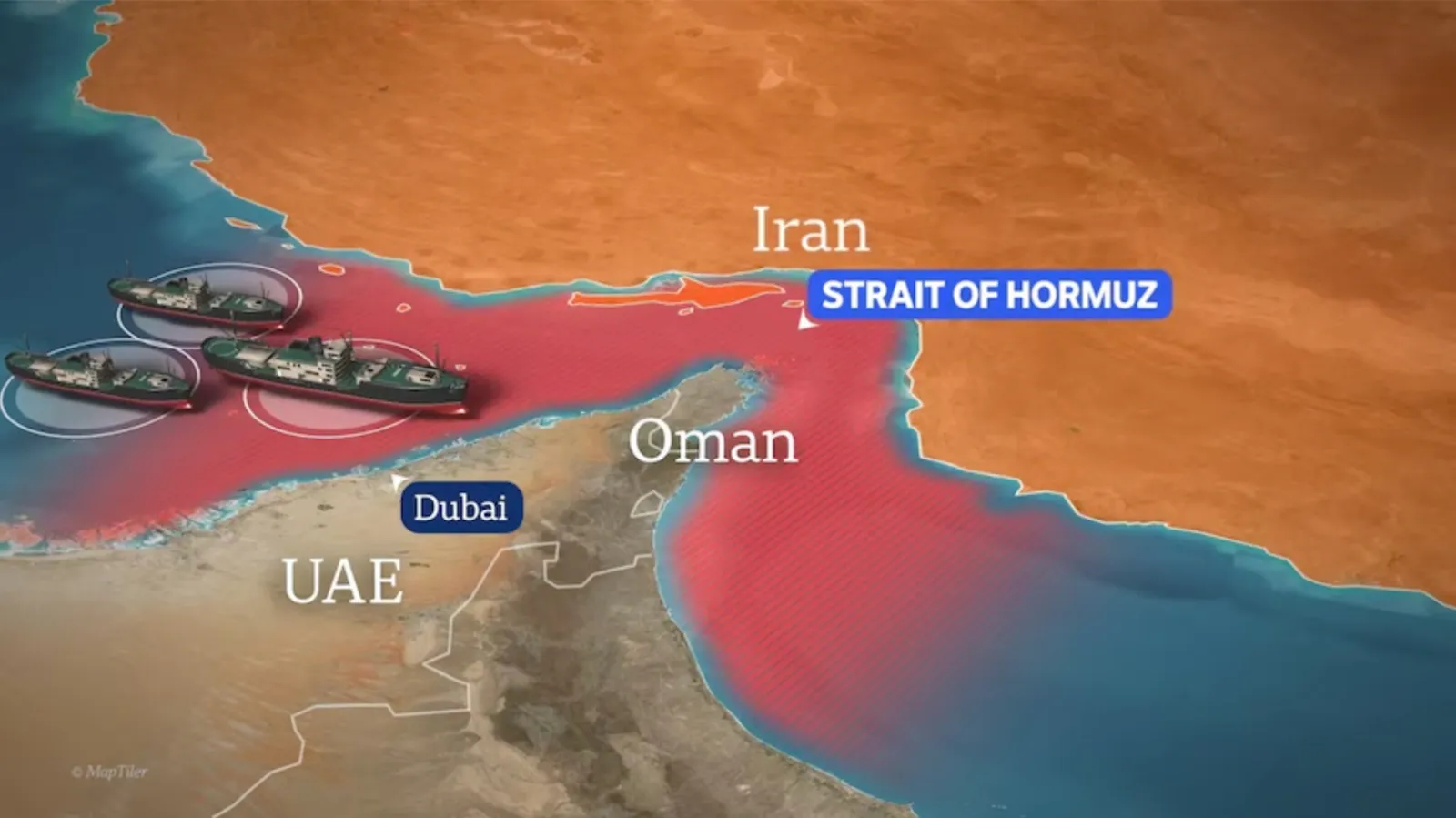

3. Fuel Security

Another major focus of the budget is increasing Australia’s fuel security and self-sufficiency amidst global oil supply disruptions.

Source: ABC

A reduction in global oil supply places upward pressure on oil prices, as demand exceeds available supply. Due to Australia’s heavy reliance on imported fuel, this can lead to imported inflation. Since fuel is a key input in production and transport, higher fuel prices raise business costs across many industries, contributing to cost-push inflation as firms pass these costs on to consumers. This may also increase inflationary expectations, as firms pre-emptively raise prices and workers demand higher wages to protect their real incomes. If sustained, this can create a wage-price spiral, further reinforcing inflationary pressures.

Inflation is measured in two ways, headline inflation and underlying inflation. Headline inflation reflects changes in the overall prices of a weighted basket of goods and services making up the Consumer Price Index (CPI), while underlying inflation excludes volatile items to more accurately reflect general price levels. Although volatile fuel prices are only directly included in headline inflation, they can still influence underlying inflation by raising production and transport costs, flowing through to a broad range of goods and services.

Additionally, by weakening real disposable income and consumer confidence, higher fuel prices cause lower aggregate demand, slowing economic growth and increasing cyclical unemployment. The budget reflects this risk, with growth projected to slow to 2.25% in 2025-26 and 1.75% in 2026-27. This indicates possible stagflation, where prolonged global supply shocks may cause high inflation, low economic growth and rising unemployment to occur simultaneously. Stagflation is particularly challenging for macroeconomic policy to address, as contractionary policies designed to reduce inflation, will weaken economic growth further.

Low income households are also disproportionately affected by rising prices, as they spend a larger share of income on essentials such as fuel and transport, exacerbating income inequality.

The government has introduced several policies to strengthen domestic fuel security, including a

$3.2 billion Australian Fuel Security Reserve to store 1 billion litres of diesel and jet fuel and a $7.5 billion Fuel and Fertiliser Security Facility providing financial assistance to support fuel storage and supply. The Minimum Stockholding Obligation is being increased by 10 days, including the amount of fuel stocks required to be held by importers and refiners. Further, gas exporters will be required to supply the equivalent of 20% of exports to the domestic market from July 2027. These aim to limit Australia’s vulnerability to further global supply disruptions and resulting broad economic harms!

However, Australia’s structural dependence on imports, reinforced by the closure of six of Australia’s eight oil refineries since 2003, limits the overall effectiveness of these policies in fully insulating Australia from global energy shocks.

Sources: Budget 2026-27, Reserve Bank of Australia, CommBank, ABC, SBS

4. Environmental Sustainability

Compared to previous years, environmental sustainability appears to be a lower priority within this budget. Environmental sustainability involves preservation of the natural environment to achieve ecologically sustainable development (ESD), which requires us to meet the needs of the present without compromising the ability of future generations to meet their own needs. This typically requires a trade off with economic growth and other short term economic objectives, as increasing sustainability requires policies which often constrain output.

The government has constrained some environmental policies in the 2026-27 budget. The Fringe Benefits Tax exemption for electric vehicles (EVs), limiting employer taxation on EVs provided to employees, has supported the uptake of 100,000 vehicles, contributing to reduced emissions. However, it is now being gradually phased down to 75% of the standard tax rate. Additionally, funding for Round 2 of the Hydrogen Headstart Program has been halved to $1 billion, reducing financial support for large scale renewable hydrogen projects.

The winding back of these policies reflects the political constraints affecting government decisions and the conflict between objectives, as the government is evidently prioritising short-term concerns of sustainable growth, price stability and cost of living relief over environmental investment. In the long term, this undermines environmental quality and therefore ESD by reducing standards of living and limiting productive capacity as resources are depleted.

Sources: Budget 2026-27, Australian Financial Review, UNSW

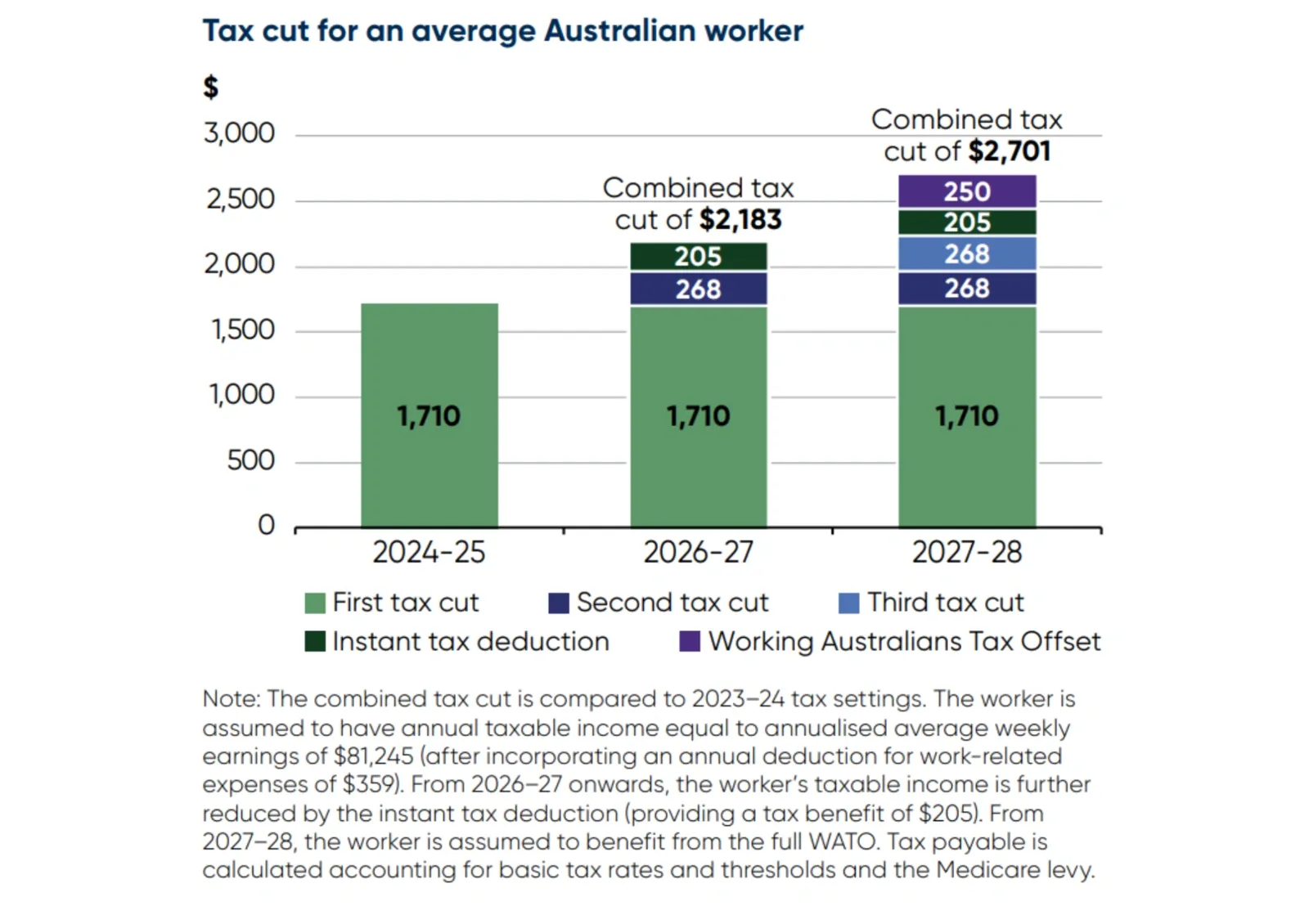

5. Income Tax Relief

The budget also attempts to address cost of living pressures through targeted income tax relief. This includes a $250 Working Australians Tax Offset from 2027-28 and a $1000 instant tax deduction from 2026-27, allowing eligible workers to easily deduct work related expenses from taxable incomes. In combination with tax cuts introduced in previous budgets, an average worker could receive tax savings up to $2183 in 2026-27.

This creates increased disposable income for individuals, reducing cost of living pressure and improving the distribution of income and wealth, as the cuts make up a greater proportion of lower incomes. Further, tax relief targeting lower income workers who have a high MPC can stimulate consumption and aggregate demand and therefore achieve economic growth.

However, ongoing inflation leads to ‘bracket creep’, where wage increases cause workers to move into higher tax brackets without experiencing real wage growth, as the prices of goods have also increased. The Australian Financial Review projects that by 2031-32, households will ultimately pay $2,398 more in annual income tax compared to 2025-26. Therefore, these tax cuts may ultimately be insufficient to actually reduce tax burdens and thereby effectively redistribute income and stimulate consumption.

Sources: Australian Financial Review, Budget 2026-27

6. NDIS & Social Services

The government is seeking to reduce spending growth within the National Disability Insurance Scheme (NDIS) through tightening eligibility criteria and expanding oversight, with projected savings of $37.8 billion by 2030. Reduced spending improves the government’s fiscal position, allowing for investment into productive areas such as infrastructure, contributing to long term rises in aggregate supply and therefore economic growth.

However, limiting NDIS access risks increasing inequality in the distribution of income if vulnerable individuals lose affordable access to essential services, as an estimated 160,000 people will lose eligibility.

Nevertheless, the government has expanded spending in other social service areas. This includes $2 billion into the Thriving Kids Program to support children with development delays, $5.9 billion to expand the Pharmaceutical Benefits Scheme, $25 billion into public hospitals, and $11.4 billion to increase bulk billing incentives, reducing healthcare costs.

These policies contribute to greater equity by redistributing income through the taxation system, as tax funds collected from high income earners are invested into public services, which disproportionately benefit low income earners who would otherwise spend a substantially larger proportion of their income on essential services.

Sources Budget 2026-27, UNSW, The Guardian

Overall, this budget introduces major changes that are likely to influence the Australian economy in a range of ways across the short, medium and long term. However, the government faces ongoing challenges in balancing economic objectives. Continuing to keep an eye on economic statistics, projections and commentary by the government, the RBA, economists and the media will allow you to further evaluate the impact of these policies on the economy.

![[HSC] Economist: 5-12 July: Globalised Financial System, Economic Multiplier and Social Housing](/assets/blog/hsc-economist/hsc-economist-5-12-july-globalised-financial-system-economic-multiplier-and-social-housing/image.webp)

![[HSC] Economist: 15th November](/assets/blog/hsc-economist/hsc-economist-15th-november/image.webp)

![[HSC] Economist: 7-14 June](/assets/blog/hsc-economist/hsc-economist-7-14-june/image.webp)

![[HSC] Economist: 1st November](/assets/blog/hsc-economist/hsc-economist-1st-november/image.webp)